Casey

Files: The Second Crash - On the Way and Unstoppable Doug Hornig

Editor, BIG GOLD

May 29, 2009

Tuesday,

October 9, 2007 started as a nice day in New York City. A

lovely early fall day, with the temperature still a balmy

80° at 2:00 in the morning. By evening, though, the temperature

had dropped twenty degrees, the clouds had rolled in, there

was thunder and rain.

As with the weather, there were some hints of trouble here

and there on Wall Street. But all in all, things could not

have seemed better. Little did we know, the stormy end of

10/9/07 signaled a very large bubble that had just popped.

That was the day when the Dow Jones Industrial Average hit

its historic peak. From there, it was all downhill - slowly

but steadily at first, and then violently after last August

- until the Dow bottomed (for now) on March 9 of this year.

Over that span, the index lost 54% of its value.

It's been a crushing blow to just about everyone. But it's

already being referred to as the crash. As if the unpleasantness

were now all behind us. More likely, in the future it will

be seen as, simply, the first crash.

Don't believe it? In a moment you will, when you see the

scariest graph of the year.

But let's quickly recall what's already happened. During

the late, great housing boom, interest rates were at microscopic

levels, while bankers were encouraged to grant home loans

on little more than a wink and a nudge. In order to inflate

their balance sheets, those bankers resorted to all sorts

of gimmicky, adjustable rate mortgages (ARMs), whose common

feature was an interest rate that would eventually reset.

That is, it would balloon somewhere down the road. And those

most likely to come quickly to grief were the riskiest borrowers,

who held loans known as "subprime."

"But not to worry," borrowers were told. "Betting

on ever-rising home prices is the safest wager in the whole

wide world. If you have problems with cash flow when the ARM

resets, your house will be worth a lot more, so you can simply

sell it and walk away with a nice chunk of change in your

pocket." Uh-huh.

The bankers themselves were a little more concerned about

the deterioration of their portfolios. They took out insurance

in the form of credit default swaps (CDSs). These were a brand-new

invention in world financial history, allowing mortgages to

be sold and resold until they were leveraged 20 times over.

They became the shakiest part of a huge global derivatives

market, with a nominal value in the tens of trillions of dollars.

For a while, this Ponzi scheme even worked. But then, as

they had to, the ARMs began resetting, and there were defaults.

Then more of them. Because at the same time, the housing market

was cooling off and the economy was stalling out. More and

more people were trapped in a situation where they owed more

on their home than they could sell it for. Many simply mailed

their keys to the bank and moved on.

All of this wreaked havoc in the derivatives market. Sellers

of these exotic packages could no longer establish what they

were worth. Buyers couldn't determine a fair price and so

stopped buying. As the ripples spread through the world financial

system, trust disappeared and liquidity dried up.

Now consider that the base cause for all that dislocation

was the subprime sector. And how big is that? Not very. Subprime

mortgages account for only about 15% of all home loans. Their

influence has been way out of proportion to their numbers,

because of derivatives. Here's the good news: the subprime

meltdown has about run its course. These loans were resetting

en masse in 2007 and the first eight months of '08. Now they're

pretty much done.

And the bad news? No one in the mainstream media seems to

be asking what should be a pretty obvious question: What about

loans other than subprime? Truth is, the banks didn't just

trick up their subprime loans. ARMs were the order of the

day - across the board.

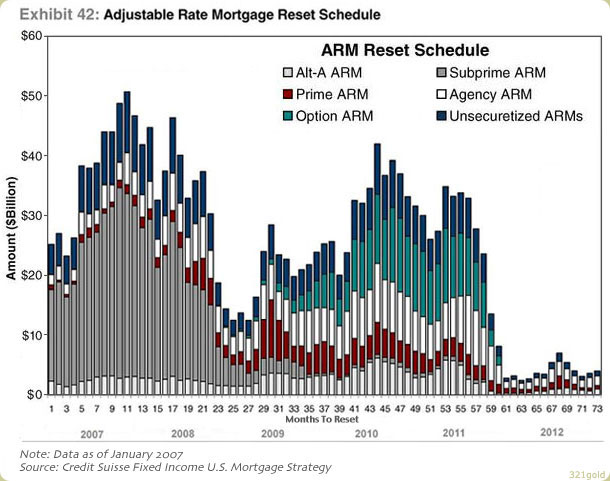

Now, here's that frightening graph we referred to earlier.

Take a good, long look. You can see that from the beginning

of 2007 through September of 2008, subprime loans (the gray

bars above) were resetting like crazy. Those are the ones

people were walking away from, sending a shockwave from defaults

and foreclosures smack into the middle of the economy. Now

they're gone.

The ARM market got very quiet between December 2008 and March

2009, hitting a low that won't be seen again until November

of 2011. Small wonder a few "green shoots" have

poked their heads above ground. But in April, resets began

to increase and will reach an intermediate peak in June. After

that, they tail off a little, going basically flat for the

next ten months.

It's not until May of 2010 that the next wave really hits.

From there to October of 2011, the resets will be coming fast

and furious. That's 18 months of further turmoil in the housing

market, and the beginning is still nearly a year away! (Although

the months in between are likely to be no picnic, either.)

While it isn't subprime ARMs that are resetting this time,

neither are they prime loans. Those eligible for prime loans

wisely tended to stay away from ARMs in the first place, as

indicated by the relatively small space they take up on each

bar.

No, the next to go are Alt-As (the white bars), Option ARMs

(green) and Unsecuritized ARMs (blue). Alt-As are loans to

the folks who are a small step up from subprime. Unsecuritized

loans are a 50-50 proposition; either the borrowers were good

enough that they weren't thrown into the CDS pool, or they

were so risky no one would insure them.

Those two are bad enough. But Option ARMs are the real black

sheep, loans with choices on how large a payment the borrower

will make. The options include interest-only or, worse, a

minimum payment that is less than interest-only, leading to

"negative amortization" - a loan balance that continually

gets bigger, not smaller. Imagine what happens with those

when the piper calls.

Once the carnage begins, will it be as bad as the subprime

crisis? That's the $64K question. Perhaps not. For one thing,

subprime loans were a much larger chunk of the market when

they started going south. For another, there's been a lot

of refinancing as interest rates dropped; that should help

ease the default rate. And the government has massively intervened,

with measures designed to prop up those who would otherwise

lose their homes.

On the other hand, we're in a severe recession, which wasn't

the case when the subprime crisis started. More people will

be unable to meet payments. And the housing market has continued

to decline, pressuring both marginal homeowners and banks

that can't sell foreclosed properties.

Is the stock market's next 10/9/07 on the way? Yes. Which

day will it be? That's unknowable. It could be in a week,

or not for another year.

But make no mistake about it, the second crash is coming.

It can't be prevented, no matter what desperate measures Obama

and his hapless financial advisors come up with. All we can

hope for is that, with a little luck, it won't be as severe

as the first one. But it will last longer. We aren't even

in the middle of the woods yet, much less on the way out.