Could Trump Bring

Back the Gold Standard? by Mark Nestmann

| March 15, 2017

Imagine the world in which

the president of the United States decides that the government

will set wages and prices. One evening, the president announces

to the nation:

“I am today ordering a freeze on all prices

and wages throughout the United States.”

After a short transition period, any increases

in wages or prices would need to be first approved by the

government.

What would happen next? We don’t have to

look very far to see the consequences of such actions. That’s

because, on August 15, 1971, President Richard Nixon made

that exact announcement.

The results were disastrous. Farmers stopped

shipping out their crops for processing. Manufacturers laid

off workers and cut output. Food shortages quickly developed.

When Nixon stated this declaration, I was

a teenager. While my mother initially thought price controls

were a wonderful idea, she changed her mind only a few weeks

later. She found out that she could no longer buy her favorite

brands in stores. Manufacturers realized they could not

make a profit by delivering them at a government-controlled

price.

Of course, there are many modern analogies.

For instance, Venezuela has had stringent price controls

in effect for over a decade. Not surprisingly, supermarket

shelves have been empty for years. There are pervasive shortages

of food, medicine, and other necessities.

Most of us almost instinctively recognize

the folly of wage and price controls. Yet, we’re perfectly

content to have the government control the nation’s monetary

system. This occurs through the Federal Reserve, which sets

short-term interest rates and periodically injects “liquidity”

into the marketplace to cope with financial crises and acts

as a lender of last resort.

The Fed’s policymaking decisions are made

in periodic meetings of its “Open Market Committee.” The

committee consists of 12 members – the seven members of

the Fed’s Board of Governors; the president of the Federal

Reserve Bank of New York; and four of the other 11 other

Reserve Bank presidents.

In other words, the monetary policy of the

US – the world’s largest economy – is effectively controlled

by 12 people.

According to the Federal Reserve Act, the

“monetary policy objective” mission of the Fed is to:

… promote effectively the goals of maximum

employment, stable prices, and moderate long-term interest

rates.

So, how well has the Fed accomplished these

goals? Let’s focus on the issue of “stable prices.”

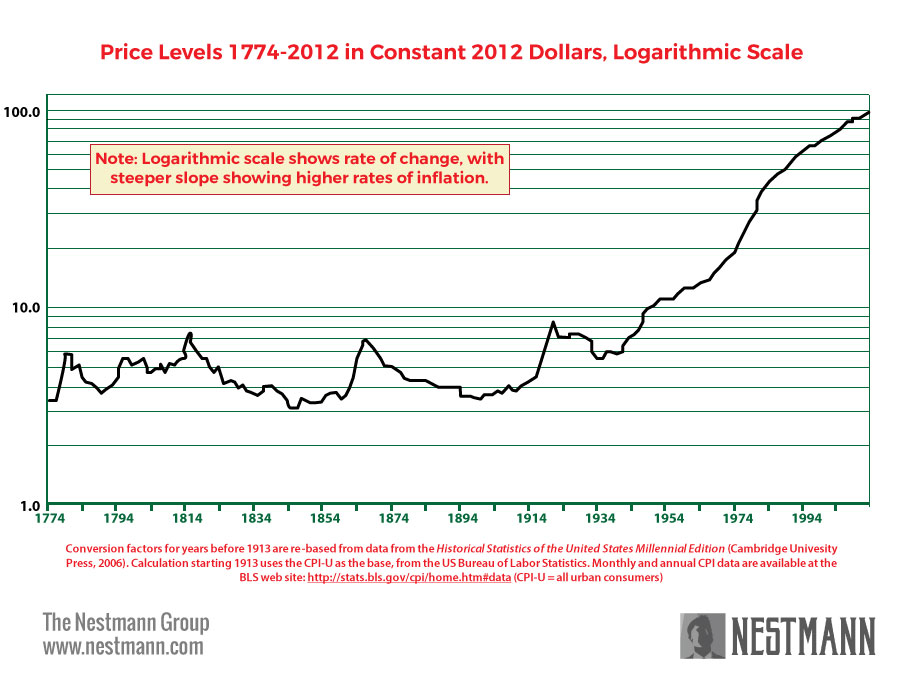

The graph you’re viewing is a historical

record of US price inflation from colonial times to the

present day. Note that price levels in the early 20th century,

before the Fed came into existence, were roughly the same

as they were in colonial times. What mechanism kept prices

stable, if not a central bank?

In the first 130-plus years of US history,

America operated on a “gold standard.” In other words, the

value of a dollar was defined in terms of gold, and anyone

who held dollars could exchange those dollars for gold.

At times the country used a bimetallic – gold and silver

– standard. At the same time, the US dollar wasn’t “legal

tender” – if you didn’t want to accept dollars as payment

for your goods or services, you didn’t have to. You could

demand payment in gold, silver, or even accept payment in

private currencies issued by many of the country’s banks.

In other words, there was competition for

money. Nor was there a mechanism in place for a lender of

last resort to “inject money” into the system, as the Fed’s

mandate permits it to do.

As the graph demonstrates, this system worked

superbly at controlling inflation. Once a committee of 12

started calling the shots, however, inflation began to rise

at almost an exponential rate.

For decades, discussion of a return to the

gold standard has been mostly restricted to earnest discussions

among libertarians. Occasionally, a professor publishes

an article on it in a seldom-read publication. But that’s

starting to change, thanks to a statement President Donald

Trump made during his campaign. In a March 2016 interview,

he said:

“We used to have a very, very solid

country because it was based on a gold standard… Bringing

back the gold standard would be very hard to do, but boy,

would it be wonderful. We’d have a standard on which to

base our money.”

I don’t know how much President Trump actually

knows about the gold standard, but his statement is factually

correct. Ending the Fed’s monopoly over money and interest

rates would be hard to do, but it could go a long way toward

fulfilling his promise to “make America great again.”

But what, exactly, would have to happen

for this to occur?

First, Congress would need to abolish the

Fed. There’s little political will to do that now, other

than a few Tea Party Republicans willing to at least entertain

the idea.

That’s just for starters. Congress would

also need to redefine the dollar in terms of a unit of gold

– establish a price point for which the Treasury would be

obligated to exchange gold for dollars. And because a gold

standard works well only when all major countries adhere

to it, the US would need to persuade its major trading partners

– think China, Canada, the EU, and others – to go along

with it.

That might not be as hard to accomplish

as you think. The dollar is already effectively the world’s

reserve currency. Backing it with gold wouldn’t change that

status, other than making it more attractive. Many countries

also effectively link their own currencies to the dollar,

including China and much of Central and South America.

The biggest political obstacle to overcome,

though, will be the ingrained belief that in a financial

crisis, there must be a lender of last resort. To that,

I would simply say, “Why?”

In the financial crisis that began in 2007,

numerous banks, financial institutions, insurance companies,

and manufacturers were effectively bailed out by the Fed.

They carried out risky lending and underwriting practices,

knowing that if a crisis occurred, they could expect a handout.

Critics say that in a world with a gold

standard, insurance giant AIG would have collapsed. So would

nearly all of Wall Street’s mega-banks, most US auto manufacturers,

and many other companies. The recession would have quickly

turned into a depression, with cataclysmic results for the

economy.

But that’s missing the point. In a world

with a gold standard, the financial excesses that brought

about the events beginning in 2007 would never have occurred.

If your business isn’t expecting a handout if and when times

get rough, you tend to operate it more prudently.

Perhaps the best argument for a gold standard

came from former Fed Chairman Ben Bernanke, who, paradoxically,

opposes it. In testimony before Congress in 2011, he was

asked, “Why do people buy gold?”

Bernanke’s reply: “As protection against

of what we call tail risks: really, really bad outcomes.”