Is

it time to buy back into gold? As stock markets wobble, investors

are taking a second look at the embattled safe haven by Eleanor Lawrie

For Thisismoney.co.uk | Published: 06:15 EST, 26 January 2016

| Updated: 10:07 EST, 26 January 2016

- Gold hit a five-year

price low in November last year, meaning it could be an

opportunity to buy in

- Ongoing volatility in financial markets could increase

the allure of gold, which tends not to rise and fall with

other assets

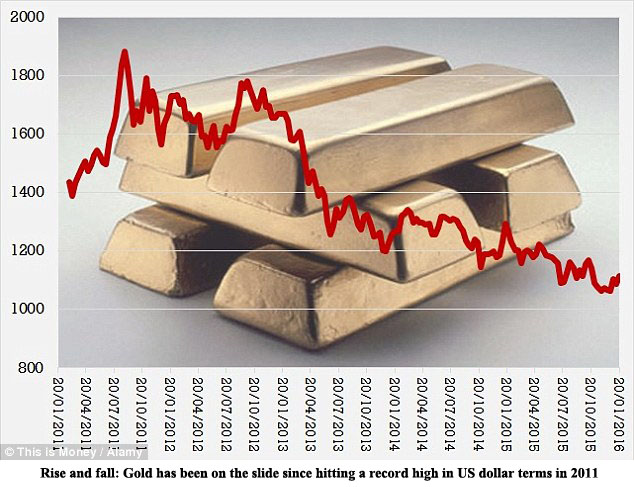

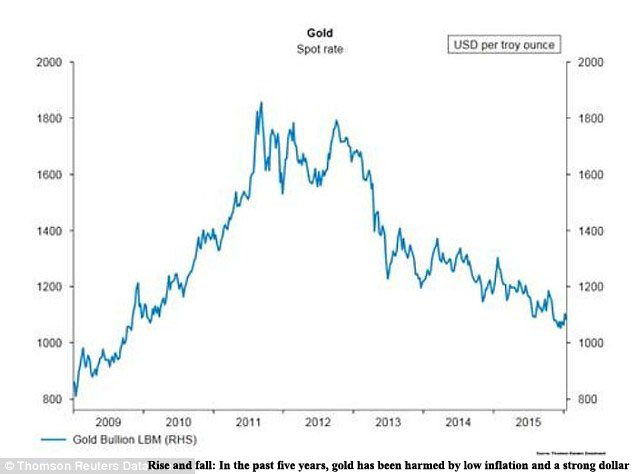

The last five years have

not been kind to gold, with the price falling steadily since

the middle of 2011

But the traditional safe haven commodity's

fortunes could be looking rosier as investors search for

shelter from the current volatility in financial markets.

The FTSE All-World index had its worst start

to the year in two decades, while the FTSE 100 briefly dipped

in to a bear market last week, dropping more than 20 per

cent below its all-time high last spring.

By comparison, since the start of 2016 the price of gold

has risen by 5 per cent, although it is still subdued compared

to its all-time high.

Gold is currently trading at $1,114 - down

42 per cent in US dollar terms on the $1,921 high in September

2011.

Maike Currie, investment director at Fidelity

International, says the headwinds surrounding gold are short-lived:

'Market turbulence and geopolitical uncertainties

are bound to drive risk-shy investors to gold given its

status as safe haven asset. Investors buy the yellow metal

during times of market panic because it seen as a store

of value.

'In recent years gold has been hurt by low

inflation and the strength of the dollar but these short-term

headwinds could dissipate and the low gold price should

stimulate demand.'

She suggests the growing change in sentiment

towards gold could gather momentum.

'As investors concerned about market volatility

move towards it, they bid up its price, justifying the initial

rush and encouraging others to do the same.

'The biggest risk to gold overall is an

increase in real interest rates. If this happens the opportunity

cost of holding gold will encourage investors to sell the

metal. But Mark Carney has made it very clear that rates

will stay lower for longer.'

In theory, the gold price should have taken

a hit from the US Federal Reserve's decision to raise interest

rates last month, as a stronger dollar weakens the case

for holding the asset class - and as gold in priced in US

dollars it makes it more expensive.

But instead the price has started to tentatively

rise. One reason is market volatility, crude oil recently

hit a 13 year price low, while concerns about a potential

devaluation in the Chinese yuan also weigh heavily on investors'

minds.

Adrian Ash, head of research at BullionVault,

suggests holding part of your portfolio in gold could be

a good insurance policy if markets do continue to fall.

'Gold tends to do well when other things

don't, and vice versa, which is why the price has fallen

by 40 per cent since 2011.

'For the long term it's useful if you think

things will go badly wrong. There is a lot of anxiety and

trouble out there today and if you are anxious about the

outlook for equities, and particularly the pound, in terms

of a sterling hedge it's worth looking at gold.'

'Everybody thinks gold is going to become

a consensus story but the fact is it is still out of favour

in terms of being a consumer play.

'Gold is a form of insurance and you obviously

want to buy when prices are low. Gold does cost you - if

you put 10 per cent in gold and everything else does well,

then you won't do as well - but that's the price of having

insurance.

'Plus, you want to buy insurance when it's

cheap, and this is one of the cheapest times you can buy

in.'

But Stephen Jones, chief investment officer

at Kames, argues that despite the tone of market uncertainty,

the appeal of gold remains limited .

'The price of gold has reacted only modestly

to the upheavals in markets seen in the short time since

New Year. You can argue it has been something of a hedge

against volatility, but the moves have been only modest

and not enough to begin to offset price moves in other assets.

Looking at the wider context, he doesn't

think it's a good time to move in to the asset class.

'Longer term you can't ignore the fact that

the gold price has been falling consistently for the last

three years. Compared to this time last year, gold is $200

per ounce lower in price.

'We don't see this longer term trend coming

to an end just yet. First and foremost gold is a hedge against

inflation, and the outlook for inflation remains very subdued.

Recent data from the UK, Europe and the US reports little

or no movement in prices over the past year, and the outlook

is for more of the same.

'In this environment large scale price appreciation

for gold seems remote and we continue to avoid the commodity

for now.'

And Hector McNeil, co-CEO of ETF specialist

Wisdom Tree Europe, goes even further, saying he doesn't

think gold would offer even limited protection from a market

rout.

'We are in bear market territory for equity

markets and investors think of gold as a safe haven so it

may get some interest. But gold is not a safe haven. Gold

has done nothing but fall over the past few years, despite

numerous sell-offs for markets. If it was a true safe haven

the price would have risen during periods of stress.

'For example, during the 2013 debt-ceiling

crisis in the US, when the world's largest economy was on

the brink of defaulting, treasury yields spiked. Despite

growing fears about the impact of a default, the price of

gold barely moved, and indeed if you look at it over history

it has never acted as a safe haven asset.'

He notes that the growth of exchange-traded

commodities gave investors far better access to the asset

class.

This, combined with the commodity's increasing

popularity in China, helped cause a decade-long rally. But

those themes have already played themselves out.

He says: 'We cannot see where the spark

will come from for gold, and most allocations to the precious

metal within portfolios are fairly static, so we do not

expect it to rally.'

What is the best way to invest in

gold?

If you believe the yellow metal is about

to see a turnaround in its fortunes, or that it could be

a useful hedge if the wider economic situation continues

to deteriorate, there are several ways to get involved.

One way is through holding gold bullion,

or physical gold.

The advantage of holding physical gold is

that it gives you direct control over your investment. The

disadvantage is that it comes with storage, transport and

insurance costs. For these reasons, physical bullion has

traditionally been dominated by institutional investors

or central banks who buy in very large amounts.

Smaller investors who want to buy physical

need to contact a dealer, who may also be able to help store

it for them. They can buy either buy gold in bars, or coins.

Over the past decade, it has got easier

and cheaper to buy and store physical gold. Companies such

as ATS Bullion, Chards, Baird & Co, BullionVault and

GoldMadeSimple allow investors to buy gold in varying amounts

and different forms online and can arrange storage.

Exchange traded fund providers pool investors

cash together and offer direct exposure to a fund that tracks

the gold price.

Investors should check costs and whether

the funds either track gold through holding physical bullion,

or are synthetic and replicate it with derivatives - these

carry extra risk in that the counter-party in the derivatives

trade may find itself unable to fulfil its commitments.

There are also diversified commodity indexes

which hold a proportion in gold. These 'broad basket' ETCs

track an index including all the major commodities across

energy, metals and agriculture.

Another advantage of investing through an

ETC is they are a more liquid form of investment than a

direct ownership of physical gold because they are traded

daily on stock exchanges like shares - allowing investors

to easily buy or sell.

Alternatively, a more diversified way to

access gold is through an actively managed fund such as

the BlackRock Gold & General, or Investec Global Gold,

which invest in gold mining companies rather than gold bullion

itself.

Both saw their share price dip by 25 per

cent last year, but are two of the funds regularly tipped

by those who believe the gold price will rally.