Peak Gold – Did

Gold Production Peak in 2015? by Mark O'Byrne |

August 1, 2016

‘Peak Gold’ is happening

which has important ramifications for the gold market and

is another long term positive fundamental. This is why we

were one of the first analysts to consider the peak gold

phenomenon back in 2007 and 2008 and have considered peak

gold frequently over the years.

One of the more astute gold

analysts today, Frank Holmes also believes that peak gold

is happening and may even have occured in 2015. Peak gold

and the fact that total annual global gold production is

likely to have peaked is an important supply side factor

in the gold market. This is one of the bullish factors which

will support prices and indeed should contribute to higher

prices in the coming years.

Holmes latest article is a must read:

The Last Known Gold Deposit

Gold is one of the rarest elements in the

world, making up roughly 0.003 parts per million of the

earth’s crust. (For some perspective, one part per million,

when converted into time, is equivalent to one minute in

two years. Gold is even rarer than that.) If we took all

the gold ever mined—all 186,000 tonnes, from the bullion

at Fort Knox to India’s bridal jewelry to King Tut’s burial

mask—and melted it down to a 20.5 meter-sided cube, it would

fit snugly within the confines of an Olympic-size swimming

pool.

The yellow metal’s rarity, of course, is

one of the main reasons why it’s so highly valued across

the globe and, for most of recorded history, recognized

and used as currency. Unlike fiat money, of which we can

always print more, there’s only so much recoverable gold

in the world. And despite the best efforts of alchemists,

we can’t recreate its unique chemistry in a lab. The only

way for us to acquire more is to dig.

But for how much longer?

Goldman Sachs analyst Eugene King took a

stab at answering this question last year, estimating we

have only “20 years of known mineable reserves of gold.”

The operative word here is “known.” If King’s

projection turns out to be accurate, and the last “known”

gold nugget is exhumed from the earth in 2035, that won’t

necessarily spell the end of gold mining. Exploration will

surely continue as it always has—though at a much higher

cost.

(In fact, our insatiable pursuit of gold

might one day soon take us to space, as President Barack

Obama signed legislation in November that permits commercial

mineral extraction on asteroids and the moon. Many near-Earth

asteroids are said to contain trillions of dollars’ worth

of precious metals and other minerals. But that’s a discussion

for another time.)

We’ll probably see a surge in mergers and

acquisitions, as I told Kitco News’ Daniela Cambone last

week. I think that as long as they have reliable output,

mid-cap companies could be gobbled up by the Barricks and

Newmonts of the world.

Another consequence of recovering the last

known nugget? The gold price could spike dramatically to

levels only imagined. My colleague Jim Rickards, in his

book “The New Case for Gold,”puts it at $10,000 an ounce.

GoldMoney founder James Turk says it’s closer to $12,000.

There’s really no way of knowing how high gold could go.

Did Gold Production Peak in 2015?

What we do know is that global gold output

has been contracting since 2013. Last year might have been

the tipping point, however, in line with Goldcorp CEO Chuck

Jeannes’ prediction that peak gold was within spitting distance.

“There are just not that many new mines

being found and developed,” he told the Wall Street Journal

in 2014, adding that this was “very positive” for the gold

price going forward.

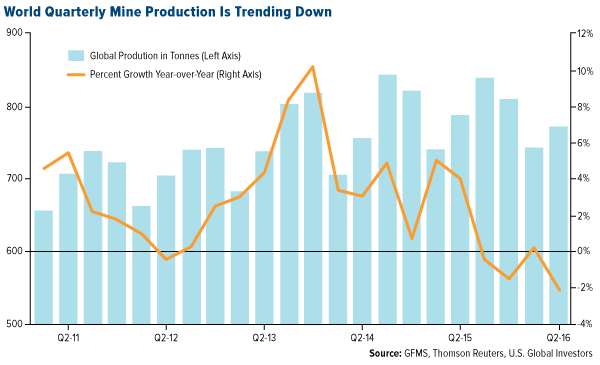

This year, second-quarter mine supply was

2 percent less than the same period in 2015, according to

preliminary estimates made by Thomson Reuters GFMS. Some

analysts now expect global production to fall 3 percent

in 2016, after seven straight years of growth.

What’s more, few new projects and expansions

are expected to come online this year, writes Thomson Reuters,

“and those in the near-term pipeline are generally fairly

modest in scale, hence our view that global mine supply

is set to begin a multiyear downtrend in 2016.”

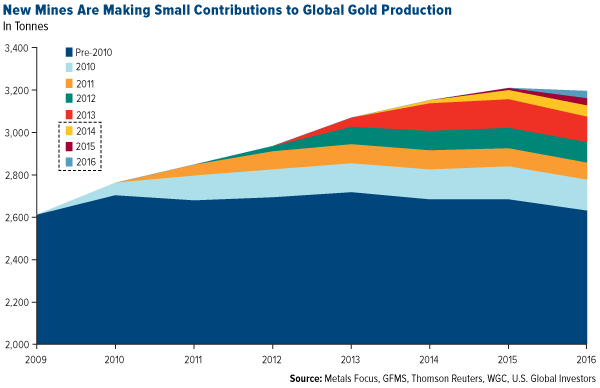

Indeed, if we look at projects that opened

in just the last two or three years, we see that they’re

of lower grade, meaning they don’t produce nearly as much

as older, easy-to-mine gold deposits.

The truth of the matter is, when it comes

to discovering new gold deposits, the low-hanging fruit

has likely already been picked. Gone are the days when someone

could stumble upon an exposed hunk of gold at the bottom

of a riverbed, as James Marshall did in 1848, setting off

the California Gold Rush. Every year, the pursuit of gold

becomes increasingly more challenging—not to mention more

expensive—requiring ever more sophisticated tools and technology,

including 3D seismic imaging, direction drilling and airborne

gravimetry. (A satisfactory “gold fracking” method, however,

seems unlikely to become reality any time soon.)

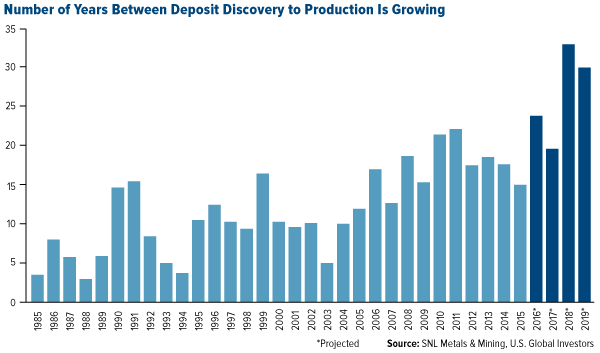

Compounding the issue is the fact that the

number of years between discovery of a new major deposit

and production is widening, due to the increase in feasibility

assessments, compliance, licenses and more—and that’s all

before nugget one can be extracted. The average lead time

for gold mines worldwide is close to 20 years, though it

can sometimes be more, depending on the jurisdiction. This

highlights the need for worldwide policy reform to remove

many of the barriers that obstruct responsible mining.

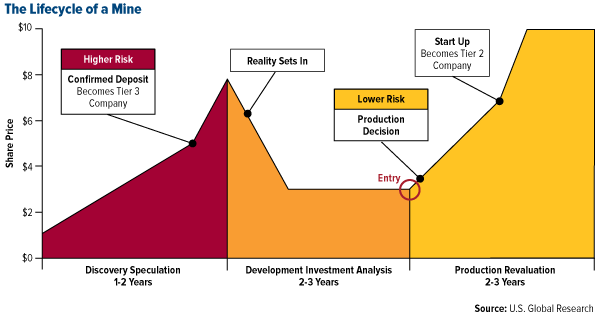

In The Goldwatcher, the book I co-wrote

with John Katz, I expressed the importance of knowing which

developmental stage of a mine’s lifecycle a project currently

falls into, as this has a strong influence on stock performance.

Investing, like life, is all about managing expectations.

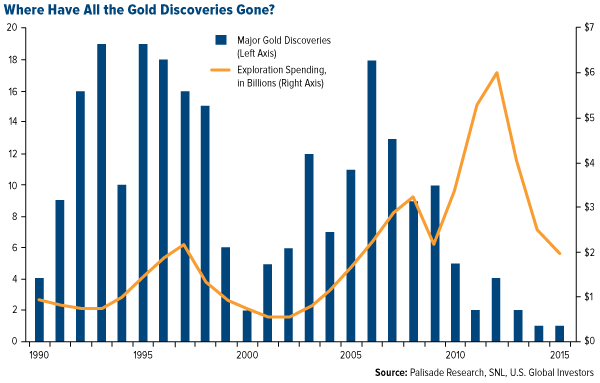

Few New Mines as Companies Deleverage

What all of this means is we’ll probably

continue to see fewer and fewer major discoveries, or those

that yield more than a million ounces. As you can see below,

new gold discoveries peaked in 1995. Exploration spending

peaked nearly 20 years later when the price per ounce averaged

$1,600.

With gold now trading above $1,340 an ounce,

up 26 percent for the year, many investors expect producers

to begin lifting spending on exploration and production

(or dividends).

Instead, most companies are in cost-cutting

mode, using this opportunity to pay down debt and liquidate

assets. According to Reuters, North American gold producers

have managed to lower their debt levels 30 percent since

late 2014.

Speaking to Mining.com, Newmont Mining CEO

Gary Goldbergsaid his company, the second-largest gold producer

in the world, is one of the few that’s currently building

new mines—specifically the Merian project in Suriname and

Long Canyon in Nevada. Because of the lack of new mines

being built, he sees supply falling 7 percent between now

and 2021.

Demand for the yellow metal, on the other

hand, should remain strong during this period, helping to

support prices even more.

Massive Inflows into Gold Funds

In the meantime, gold continues to find

support from global monetary policy and low to negative

government bond yields. Last week the Bank of England cut

rates as part of a stimulus package, which both weakened

the British pound 1.5 percent and gave the yellow metal

a jolt.

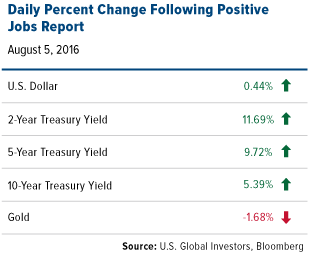

These gains were erased, however, following

Friday’s better-than-expected U.S. jobs report, which sparked

a rally in Treasuries. This contributes to the narrative

that gold and government debt are inversely related, a key

component of the Fear Trade.In the meantime, gold continues

to find support from global monetary policy and low to negative

government bond yields. Last week the Bank of England cut

rates as part of a stimulus package, which both weakened

the British pound 1.5 percent and gave the yellow metal

a jolt.

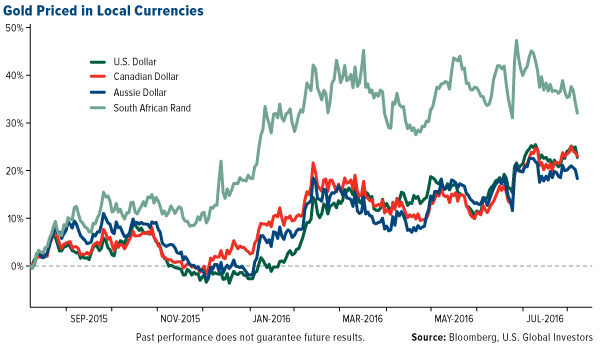

When priced in the local currencies of the

U.S., Canada, South Africa or Australia—four of the largest

gold-producing countries—bullion is up, which has boosted

miners’ profits. Gold stocks, as measured by the NYSE Arca

Gold Miners Index, have appreciated 128.92 percent in the

last 12 months.

For the first half of 2016, inflows into

commodities have been the strongest since 2009. Gold and

other precious metals account for about 60 percent of the

new money, which has pushed commodity assets under management

above $235 billion. Barclays believes 2016 could be the

best year on record for gold-related ETFs and other funds,

with many big-name hedge fund managers, from Stan Druckenmiller

to Paul Singer to Bill Gross, singing the praises of the

yellow metal.