Why Gold Could Be the Safest Investment Out There By Seeking Alpha|

October 18, 2010

A look at the past 177 years of the gold price reveals

that unexpected write-offs are non-events—gold could

be the safest investment out there.

Investing into anything is usually preceded by the thought:

what is there to win and what is there to lose? There has

been a lot of discussion about the upsides of the gold rally.

But little if nothing has been said about the potential

losses. Clearly, many people are wary of investing in gold

because they fear that the gold price could suddenly crash.

Gold has so far attracted only $5.4 billion worth of private

investment in 2010. At the same time, investors poured $22

billion into emerging market mutual funds and $155 billion

into bonds. While some commentators have labeled gold a

bubble, these numbers show the exact opposite. Being a tiny

fraction of the bond market's value, gold remains a niche

investment. The fear of the unknown holds savers away from

gold, and the media hype is not helping.

Most people perceive gold as speculative, whereas cash

(CDs), bonds, real estate and managed investment plans are

considered to be safe, conservative investments. But how

likely is a sudden crash of the gold price? If history is

any guide, it's not likely at all. In fact, gold has less

surprises for you than any of the assets mentioned above.

If you are a conservative investor, you must have a closer

look at gold.

1833-1969: Virtually no setbacks

The dollar-gold exchange rate was set to $18.93 per ounce

in 1833. Between 1833 and 1970, there was virtually not

a single notable year-on-year drop, with the exception of

1931. That year the gold price fell from $20.65 to $17.06,

a minus of 17%. But considering that in 1931 and 1932 the

general price level also dropped about 10% each of these

two years (while the gold price was set back to $20.65 in

1932), gold practically didn't lose any real purchasing

power but actually gained some during the deflationary Great

Depression.

The situation has changed since the late 1960s and early

1970s when the free gold market started to form. In 1971

the U.S. effectively abandoned the gold standard and no

longer guaranteed the fixed exchange rate of $35 per ounce.

With gold now being traded freely around the world, the

gold price became more volatile. Has gold since become a

risky investment?

1970-2010: Losses are minimal compared

to gains

Even in the post-gold-standard years, gold has never surprised

with a sudden crash. With one exception. In January 1980,

the Soviets invaded Afghanistan. The world was already shaken

by the 1979 oil crisis and the Iranian Revolution that was

drastically changing the balance of power in the Middle

East. This geopolitical earthquake made the gold price skyrocket

from $559 to $843, only to fall back to $668, all within

the one month of January in 1980. However, it is probably

safe to say that this was a very short window of opportunity

and virtually no private investors managed to buy gold at

the peak that lasted only 2 days.

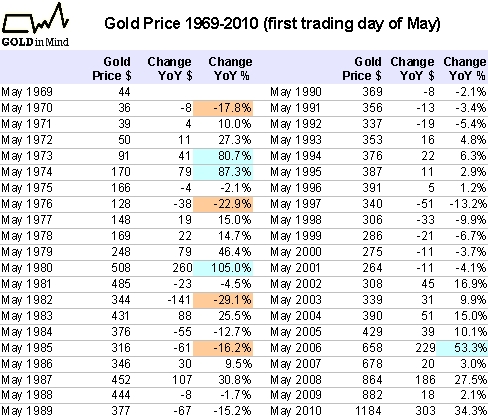

In order to study how much a typical leisure investor could

lose by investing in gold, let's consider somebody who invests

very infrequently, say once a year. Let's say our person

reserves the first workday of May for this activity. So

if he decides to buy or sell gold, he'll have to do it on

this one day of the year. For this imaginary person, I computed

gains and losses for every year since 1970 by comparing

the gold prices of the first trading day of May. Let's see

what came out (I highlighted the top four losses and top

four gains):

For our investor, the maximum loss suffered in a year in

the past 40 years was -29.1% in May 1982. Frankly, I can't

think of an investment that offers notably higher safety.

Commodities, stocks (mutual funds), cash, real estate —

all of these can lose 30% or more within a year easily.

Actually, I bet that I could find annual losses of 50% and

more in every single one of those markets in the past 40

years. Even if you think of bonds, they can still easily

lose 30% or more within a year if the currency they are

denominated in drops. The same applies to cash. If your

currency loses 30% in international comparison (which is

nothing unusual), your imports (which for many people are

the main part of their consumption) will soon get more expensive

by a similar if not greater margin.

Hence, it seems that gold is one of the most stable investments

out there. It just doesn't bust. Even after the supposed

"gold bubble" of 1980, there was no bursting.

Rather, it was a gradual deflation with enough time to get

out. Even our imaginary investor didn't suffer any notable

damage and had plenty of time to exit before making a loss.

Two more interesting things can be noticed:

Each of the top four significant losses

was followed by a year with a gain

The maximum losses are generally much

smaller than the maximum gains. While the maximum annual

loss is around 20%, the top four hikes were all above

50%. In other words, gold combines limited downside with

great upside potential

The last point mentioned is not a coincidence. It is the

key logic of the gold price: Because the amount of physical

gold available for investing is limited, any crisis in the

global financial markets usually creates a run on gold and

an over-proportionate price spike. But while financial crises

set in fast, the recovery is usually slow. A recovery is

bad for the gold price, but because it is slow, the deterioration

of the gold price is gradual. Stocks and most other markets

act in the opposite way. They grow slowly and crash fast.

The gold price "grows" fast and "crashes"

slowly. This unique inverse property of gold turns it into

an inevitable cushion for any investment portfolio.

1980s, 1990s, 2000s ... what's next?

Of course, you may argue that during the 1980s and 1990s

gold was a miserable long-term investment. I would agree

with that. Gold lost 87% of its purchasing power between

1980 and 2000. But exactly because of the property described

above, everybody had enough time to get rid of their gold.

There were plenty of signals that gold would not be a good

investment in that period—interest rates were high,

emerging economies ensured attractive returns from the stock

markets and the gold price was being watered by the central

bank gold sales. Let's compare the signals from back then

with those of today:

Signals 1980s-1990s

Fed's Paul Volcker made it clear that

he was serious about fighting inflation, raising the prime

rate to as much as 21.5%

The Soviet Bloc fell apart which created tremendous, long-lasting

tailwinds for the stock markets throughout the 1990s; Asia

was booming

The IMF and central banks were selling gold and they were

loud about it. The massive sales by the Bank of England

finally brought gold to historical lows in 2001

Signals 2010s

Fed's Ben Bernanke is not serious about fighting inflation

at all, the prime rate is to stay sub 1% and a new round

of Quantitative Easing is en route

We have no fresh emerging markets to provide expansion

and growth

Central banks will become net gold buyers in 2011, after

17 years of net gold sales

The bottom line: the signals of today are the exact opposite

of those we were seeing in the 1980s and 1990s and are telling

us to buy gold. And I haven't even touched on the topic of

our broke governments that can only pay for old debt with

printed money, thus diluting the value of cash already in

circulation. Cash, CDs and bonds are outright poison at this

point. Yet, that's where most of 401k and IRA money is. It's

sad, but what can you do. If you care about your retirement,

please have a look at gold. Remember the learnings from above.

If gold peaks, it will likely deflate slowly. Because it takes

a long time to restore sanity.

And those of you who have already been praising gold's current

prospects to your friends—why not mention the downside

the next time. It is one of the best arguments for gold.