How

do rare U.S. coins stack up as investment?

By David L. Ganz| Numismatic

News

August 7, 2007

When I first started writing

about coins professionally in 1965, the Dow

Jones Industrial Average topped out the year

at 911 on its way to 792 the following year.

Corporate bonds paid out an average of 4.49

percent according to Moody's, which quoted

the rate for corporate Aaa bonds.

Treasury bills (government

obligations of more than a month in duration)

were averaging about 3.93 percent, on their

way, thanks to the Vietnam War, to 4.76 percent

the following year, and the Standard &

Poor's 500 average was an odd-sounding.

Gold was priced at $35 an ounce officially,

and $35.15 on the free market that barely

existed, since Uncle Sam would gladly exchange

gold for dollars from anyone in the world

except its own citizens, who had all been

prohibited from owning gold (except for rare

and unusual coins) since 1933.

Silver was $1.2929 an ounce, a Rubicon of

sorts since above that price, melted silver

dollars bought at face value turned a profit

for the holder.

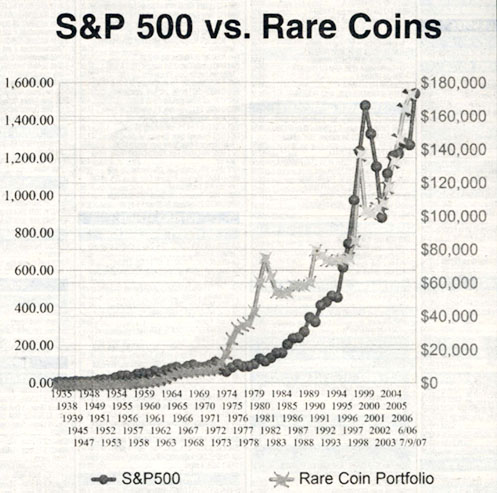

This graph compares the performance

ofthe S&P 500 stock index with that of the

rare coin market basket

Silver coin still

circulated, but barely, in 1965; by July, the Coinage

Act of 1965 ended silver in the dime and quarter and

moved toward a 40 percent silver half. By 1967, silver

ended the year above $1.55 though gold stayed at $35.

Platinum was a mere $98 an ounce (up 10.8 percent

from the previous year), and farmland in Iowa, according

to the U.S. Department of Agriculture and Iowa State

University, was selling at $318 an acre - up 9 percent

from the year before; over the succeeding 42 years

it would average advances of about 5.4 percent annually

(though obviously with some ups and downs).

Welcome to the American Numismatic Association convention

edition of the Salomon Brothers review of the corn

market, something that I've followed for more than

40 years, and written from the perspective of a collector

who also buys stocks and remembers when it made front

pages of the New York Times that the Dow had moved

downward by a mere 15 points in a single day.

As I'm writing this, the Dow has gone over 14,000

and then retreated some. My charting that accompanies

figures the Dow for what it was earlier in the summer

at 13,649. (It takes six to eight weeks to prepare

the data and then more time to do the graphing and

charts). Some of the other relevant numbers: farmland,

according to the chief professor who measures it at

Iowa State, is now going for $3,500 an acre ("or

more," he said in an e-mail interview in early

July).

Gold is figured at $661.50, up consistently since

2004; silver figures in the mix at $12.69, also a

steady price rise since 1999; platinum is figured

at $1,307 the ounce, also right up there since 2001.

The CPI is catching a little bit of inflation, averaging

about 3.43 percent annually, now at about 208 on the

1982=100 scale. OK, you want to know about where coins

stand in all this. First, a word about the portfolio

that has been averaging a 13.5 percent rate of change

since 1937 - and about 9.8 percent annually since

1965. (The Dow during the same period averaged about

7.5 percent using year-end numbers as a basis for

the average).

Both the Dow Jones and the index compilation for rare

coins utilized in this analysis use a market-basket

approach, measuring selected coins designed to represent

the whole marketplace, and selected stocks that are

broadly representative of the industrial sector of

the American economy.

Components of the Dow Jones have changed during the

period (though the results have not); the coins are

static because the index was initially compiled by

someone else and was discontinued 17 years ago. I

keep the flame alive with the original components

because it is such a good representative mix.

Dow Jones statistics are calculated daily, and based

on actual components and prices published in many

periodicals. The coin list was first compiled annually

by Salomon Brothers going back to 1978, and carried

through 1990. It was always done on an annualized

basis. That can lead to somewhat misleading results,

but still a useful analysis at a specific point in

time.

For the analysis that follows, the Salomon Brothers

raw data itself was not used; instead, both back and

forward pricing was independently examined. Coin grading

changes over the years are taken into account. The

coins, with the exception of a high-end circulated

early American copper, are either choice uncirculated

or proof (about MS-63 or Proof-63 on the numerical

grading scale); if higher grades were utilized, such

as MS-65, the results would be substantially higher.

In fact, Dennis Baker, whose NumisMedia has supplied

me with working data for the past six or seven years,

has also included MS-65 data so I can compare. It

is so off-the-chart as to make the comparisons ridiculous.

Besides, broad-based market purchases of MS-63 are

possible; by their nature, MS-65 versions of many

older rarities are either thinly traded or just not

widely available.

I said last year that a subsequent column might look

at that over the last couple of years; figure on that

to come one of these weeks. I still intend to do it

when I have some spare time, but regular readers of

this column know Kathy and I have been traveling.

Annual review of the rare coin market, contrasting

it with the rate of inflation, the price of gold and

other precious metals, and specific rare coins has

been done since the late 1970s when Salomon Brothers,

then a Wall Street powerhouse institution, did the

annual accounting and contrasted it with collectibles

and other tangible asset components across the board.

These included Chinese porcelain, stamps, farmland,

foreign exchange, vari¬ous precious metals, the

CPI and a variety of stock and bond devices. Some

of the other collectible components are not replicated

in my analysis because of the practical difficulty

in creating a database that is reliable over the extended

period of time or because they are simply areas that

I am not sufficiently familiar with.

For example, when Kathy and I traveled abroad, we

bought Chinese porcelain, but that hardly counts as

a basis of price comparison. I was able to find a

farmland index, but no luck, yet, for stamps or foreign

exchange in market basket form. I could use the Federal

Reserve Bank of St. Louis database, but not this time.

Mike Dufijj an Iowa State professor, took the time

'to provide me with good data on farmland value. I

guessed originally a 5 percent increase over last

year. He set me straight: "The bankers estimated

that our values went up 7 percent in just the first

quarter. I would think that we are probably about

10 percent up from the November estimate. That would

mean about $3,500. It could even be higher. Tilings

have slowed down a bit, but there is still a lot of

strength in the market. At a meeting I have I asked

the increase for the year and that group thought it

would be about 20 percent."

Internet research developments - not available widely

until the last couple of years - have made it possible

to use government and other statistics for farmland

value (based on average value per acre of American

farmland), corporate "Aaa" rated bonds and

other items.

This time, as in my January report, I retroactively

changed farmland to cover only that in Iowa because

the data seems more current, is reliable and accessible.

U.S. government statistics are sporadic and finalized

numbers are still two to three years old.

A total of 20 different individual coin types were

included in the Salomon Brothers examination, none

of them gold, most of them subsidiary coinage (dimes,

quarters and half dollars), some of them minor coinage

(half cent through three cent nickel) and a couple

of silver dollars and commemoratives.

Gold was left out because it was felt by Salomon that

general gold coins would mirror the gold market (a

measured component) and be influenced by non-numismatic

events. Scott Travers advanced the same argument to

me a year or so ago and I spent a hundred hours or

more to try and prove him wrong - only to discover

the data does not lie; it might work with $3 gold

pieces, but generic Saints just parallel the gold

market.

Coins included in the market basket are each broadly

representative of a class of coins, or a type that

is widely collected and hence easy to value, even

if the individual coin date and condition is not easily

replicated. For example, an 1876 20-cent piece in

uncirculated condition is approximately the same as

an 1875 20-cent piece and even an 1875-S.

A 1795 Draped Bust dollar is similar to the 1796 or

even the 1797 or 1798 silver dollar (though clearly

not the 1794, in a class by itself - you'll have to

wait for the book to see that one).

Mintages and scarcity vary, but overall trends can

be followed with reasonable adjustments. The coins

were initially selected for Salomon Brothers by Stack's,

the well-known New York coin dealer, and were designed

so that if, for example, an 1873 two-cent piece in

proof is not seen on the auction market, or in over-the-counter

trading, then an 1871 or even an 1865 (with adjustments)

can be substituted to check on the appropriate price.

I understand why a market-basket approach was initially

taken. It was in a pre-computer age except in the

most technologically advanced offices. That's the

origin of the Dow, as well; 30 numbers and calculations

are easier than 1,200. For coins, 20 is easier than

2,500.

Tracking the coins on a computerized spreadsheet has

been done by me for many years. Besides the coins,

statistics include a total amount (aggregate) for

the coin portfolio and its annual average plus rate

of change from year to year, the average price of

gold and silver, the CPI and its rate of change, gold's

rate of change, the Dow Jones Industrial average and

its rate of change and the price of platinum.

All of them initially went back to 1947, then for

several years as I got more data, back to 1938 (except

for platinum, which I initially tracked back to 1978).

I recently found good data (government mining sources)

that allowed me to value platinum for charting purposes

back to the late 1930s. I expanded coin prices back

to 1935, when Numismatic Scrapbookbegan and when reliable

auction prices made it possible to test price levels.

Last year I added University of Iowa survey going

back more than 25 years on Iowa farmland, replacing

the prior U.S. Department of Agriculture statistics

for the value per acre of farmland. It appeared in

the old Salomon Brothers survey, too, using sporadic

interpretive data. With Prof. Duffy's help, I managed

to get solid data back to 1951 (annual) and then sporadic

data back to 1935 - again, fine for charting purposes.

The average per-acre price was an average of the federal

statistics, which actually do it for each of the 50

states and make it available through the USDA Economic

Research Service and National Agricultural Statistics

Service. The current figures quoted by me are Iowa

State University's agricultural extension program.

Two years ago, I added Moody's "Aaa" rated

corporate bonds as a point of comparison, picking

up the numbers from the Statistical Abstract of the

United States, a Census Bureau-Department of Commerce

publication. Updates on this were picked up off the

Internet. The Statistical Abstract in print runs a

little behind.

I took the time to count, and what all of this means

that the current spread sheet has over 4,100 data

entry points that analyze a variety of markets. For

convenience, this year, some of the charts cover only

the last quarter century, from 1979 to the present.

Standard & Poor's, which once started in 1957,

now goes back to 1935.

There are no secrets about this; when you chart gold,

there's not a lot of movement between 1934 and 1968

- a $35 an ounce rate was enforced by the government's

purchase and sale program and by a prohibition against

domestic private gold ownership. The charts are more

interesting when looked at over the last 35 or so

years when gold or platinum are involved.

Regardless, my index points utilize the same coins

that Salomon Brothers did from 1978 to 1990, and about

which I have written extensively over that period

of time. It also utilizes the same chart and target

points - though expanded - that I've utilized in more

than 40 years of writing about the rare coin market.

Prior to 1999,1 used a wide variety of independent

sources for the chart, checking my data against reliable

price guides. Since then, Dennis Baker of NumisMedia

has been kind enough to lend me the Fair Market Value

pricing for each of the coins. Dennis used to be the

editor of the Coin Dealer Newsletter. He struck out

on his own and NumisMedia offers a fine print as well

as a fine online pricing guide (www.NumisMedia.com).

Dennis actually does the pricing (I don't go to the

Web site - we do this by e-mail) at great cost of

time and effort, and he is truly my unsung hero. Without

his help, I could never find the time to do this column

even once a year, much less twice.

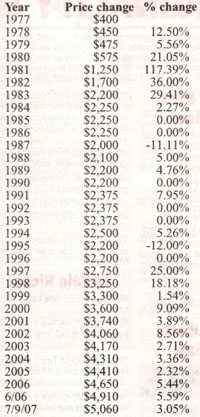

Here's an actual example of pricing for a particular

coin, the 1794 half cent in XF-40 condition, which

shows that rare coins go up, down and sideways - that

is, sometimes they don't change from year to year

at all. Even with no change, the overall picture over

a 68-year period shows an average annual return of

10.65 percent since 1935 - not bad for a circulated

coin with a mintage of over 81,000 pieces.

Take a look at the 1794 prices over the last 30 years

(from 1977):

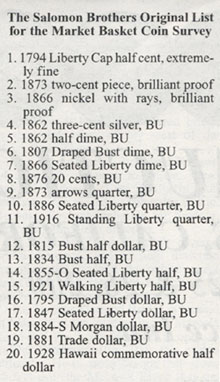

Although

the listing of the components of the Salomon

Brothers market basket was never made public

by its purveyor (Stack's, the rare coin dealership

in New York which compiled it) or the source

(the investment banker, Salomon Brothers, which

was swallowed up by Smith Barney and Citibank

more than a decade ago), the list was disclosed

in the Neil S. Berman and Hans M.F. Schulman

book on coin investing that the Coin and Currency

Institute published in 1986.

Earlier this year, a newly revised edi¬tion

of the book was published by the Coin &

Currency Institute, and it is chock full of

data and statistics. The statistics in The Investor's

Guide to U.S. Coins includes research by Dr.

Jason Perry, a financial economist at the Federal

Reserve Bank of Boston.

The coins in the Salomon Brothers report and

the report itself (which was an annual event)

took on a life of their own and made an indelible

impression on the rare coin market from 1978

to 1990. It took over the glee with which the

Red Book's annual prices were given when they

arrived on bookshelves each July 1.

(Those collectors of a certain age remember

how important Red Book price changes were -

and the reliable way that, even now, old Red

Books have come to represent a historical point

in the marketplace).

Importance of the data was heightened when the

Federal Reserve Bank of Boston published extracts

in a famous 1978 publication that called stocks-

undervalued and drew attention to the rate of

return of rare corns and other tangible assets.

The

New England Economic Review, a publication of

the Federal Reserve Bank of Boston, made the

study the focus of an article in May 1979, entitled,

"Are Stocks a Bargain?" (It concluded

that stocks were well off their historical rate

of return and hence were a bargain that a serious

investor ought to consider.).

It was given more widespread industry credence

in 1982 when A Guide Book of United States Coins,

the Red Book, published an important essay that

discussed the survey and the market-basket approach

to valuing coins as an investment. I wrote that

essay, which dis¬seminated the information

to hundreds of thousands of people.

During its dozen-year run, the Salomon Brothers

report was used in a manner similar to the Dow

Jones Industrial Average to measure growth of

selected areas of rare coins; it was a market

basket, designed to measure trends, though incidentally

it showed how several defined areas of collecting

did.

I recall calendering each year to call Robert

Salomon to both get the data and to interview

him on its meaning. (The data was initially

disseminated only to clients of the white shoe

firm, but its media life ended up giving it

greater publicity and dissemination.)

One unfortunate aspect: trends from the report

were marketed by the unscrupulous. As the Federal

Trade Commission and the American Numismatic

Association warned in a joint brochure, "Dishonest

dealers often mislead buyers by quoting appreciation

rates for rare coins from an index formerly

compiled each year by Salomon Brothers, a New

York investment bank."

The brochure continues,

"These quotes show appreciation of 12 percent

to 25 percent a year. However, the Salomon index was

based on a list of 20 very rare coins, while the coins

sold by dishonest dealers are more common coins that

are not likely to appreciate at the same rate, if

at all."

The FTC and the ANA warned that "almost all dealers,

legitimate and dishonest alike, have used the Salomon

quotes. Therefore, it is particularly important that

you choose your dealer carefully. Remember, there

is no guarantee that any coin will appreciate in value.

"

Use of the quotations and the indices was necessary

because there was no other index done by any disinterested

third party who examined the coin market, and other

points of comparison. The Salomon study was looked

at, and eagerly awaited, for as a much as it told

about coins as a it did about stocks and other investment

vehicles.

After Salomon discontinued its index and annual comparison

- under pressure from the FTC - points of comparison

were left to universal indices or even specialized

comparisons that examined the market as a whole but

failed to show earlier periods. (I've done a column

on it in Numismatic News, at least annually since

then, but the Salomon Brothers version was more universal

in its appeal and coverage).

None of the 20 coins included in the market basket

are of gem quality - the word "gem" was

used then, but not as strictly as it is today - so

most of the coins included were choice uncirculated,

the equivalent of MS-63 on most of the numerical grading

scales that are now employed, though except for coppers,

it was not in widespread use during the Salomon era.

Comparison of one or more of the coins with the portfolio

as a whole affords an opportunity to compare not only

how rare coins compare with the consumer price index

and the Dow Jones Industrial Average, but other coins

as a well - and specific issues (like, say, an MS-63

half dollar of 1921 versus an XF half cent from 1794,

and the coin portfolio average as a whole).

By 1989, the results were impressive. As the survey

written by Salomon Brothers itself stated, "Conclusion

offered: during the preceding 12-month period of time,

rare coins offered a return of more than 30 percent,"

ranking behind only old masters' paintings and Chinese

ceramics. Stocks and bonds were seriously threatened.

The accompanying charts prepared by me utilize the

20 coins that are found in the Berman-Schulman list.

Some show only from 1979 (a conceit of time) and then

show the prices for them from 1935 to the present

expressed as a total portfolio. It also shows how

the Dow Jones has done - ups, downs and all - and

compares them.

If the market basket had been compiled in 1935, it

would have cost around $125 to assemble; by 1947,

it would have cost about $430 to build the collection.

Considering that lawyers were being paid $31 a week

to work on Wall Street that year, the sum was not

inconsequential.

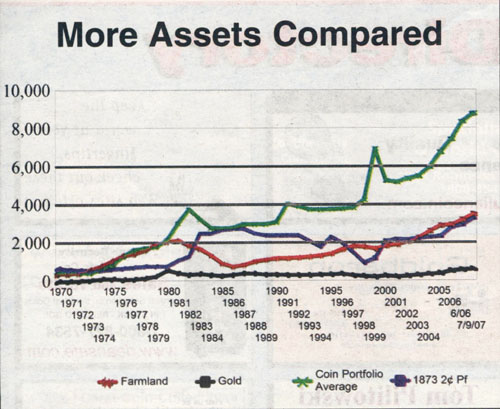

Activity since 1970 of

farmland, gold, the coin portfolio average and

the individual 1873 two-cent piece are compared.

Fast forward

some additional years. In 1956, it went over

$1,000 for the first time ($1,003) to acquire

the portfolio. By 1961, it had increased to

$2,168; in 1964 it went over $4,453 - not surprising

considering the market was fueled for success.

By 1974, the number tripled to $13,040, amidst

Nixonian inflation.

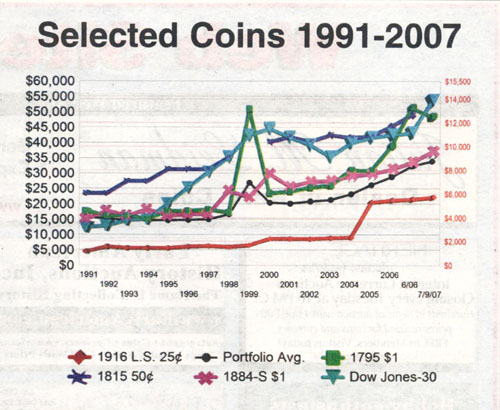

Shown from 1990 are movements of the coin

portfolio average, Dow Jones index, 1916 Standing

Liberty quarter, 1884-S dollar, 1815 half

dollar and 1795 dollar.

In 1985, a

decade afterwards, it weighed in at $54,800,

by 1997 it had increased to $74,810. The price

as of mid-2002 was $104,230 - an increase

of about 3.07 percent over the previous year.

By 2006, the value of the portfolio was $144,800.

It's now at around $170,000 and going strong.

While there's

no telling what tomorrow will bring, the charting

shows the clear past - and perhaps if trend

lines are followed, what the future might

bring